The artificial-intelligence boom has minted a clear champion. Nvidia, whose graphics processors power the training of large language models, is now worth $4.6trn, making it one of the most valuable firms in history. Yet markets often crown their winners early. If the next phase of AI is less about training models and more about running them at scale, another company—Broadcom—may emerge as the quieter giant of the AI era.

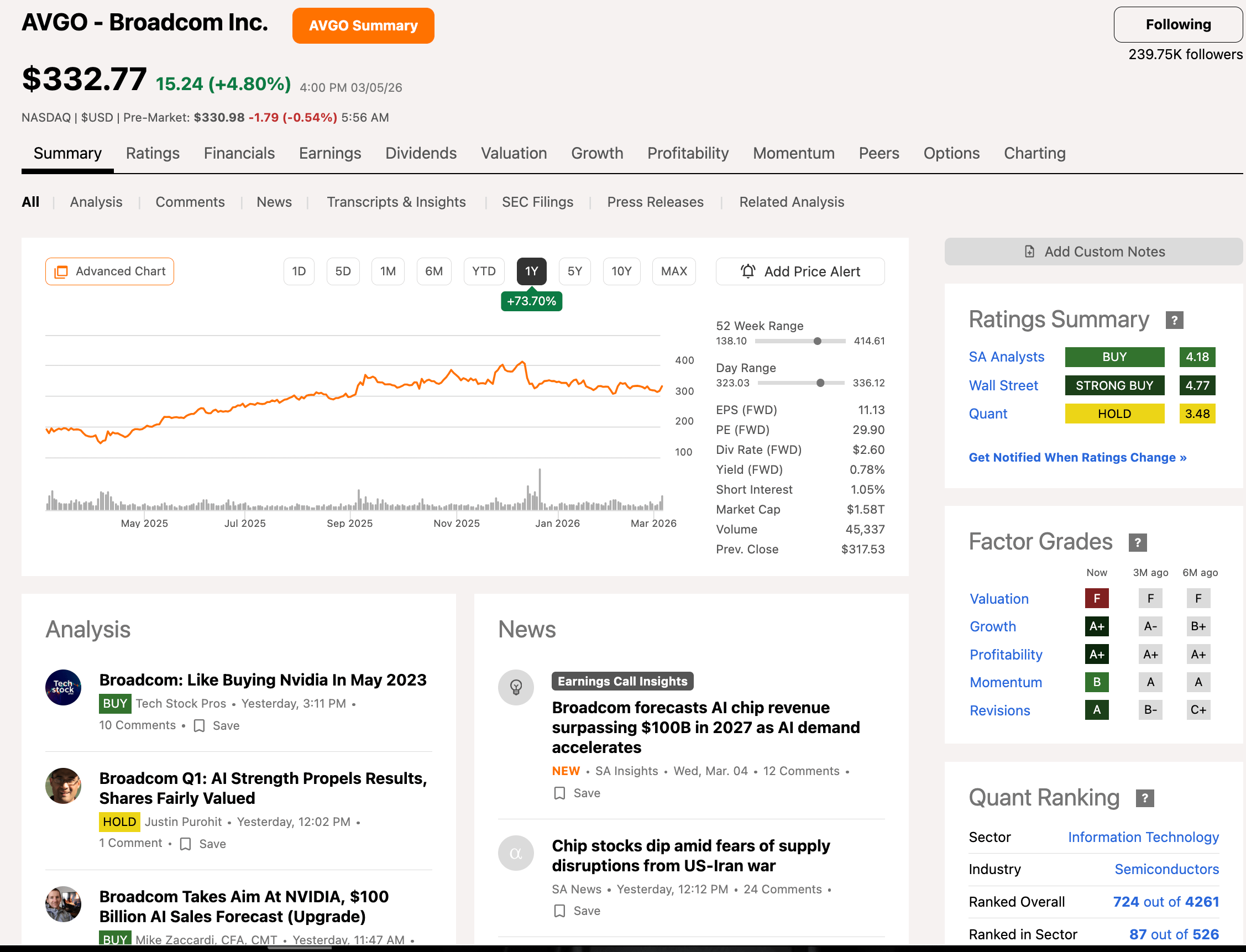

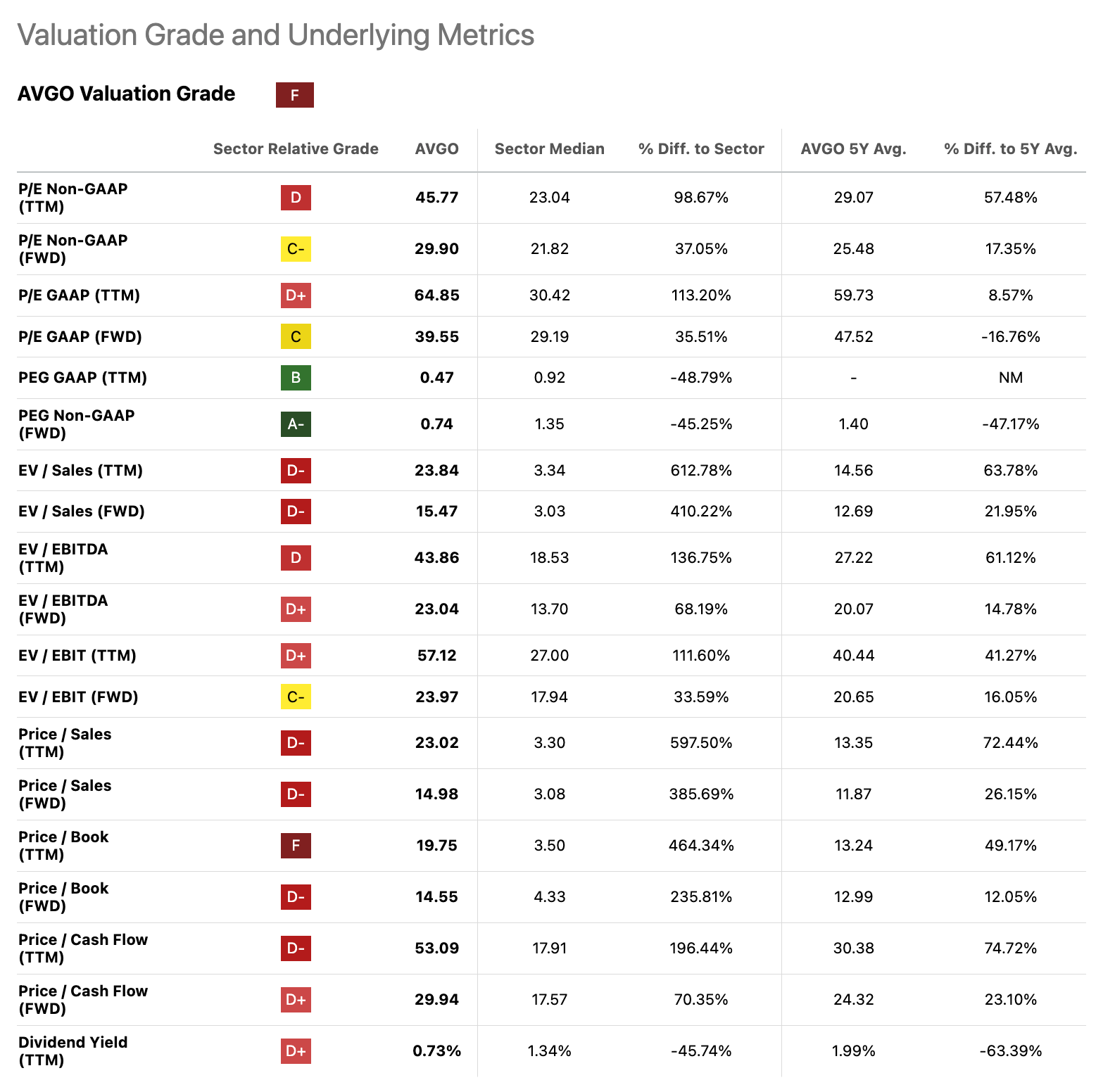

Broadcom’s current valuation already reflects the AI surge. At roughly $330 a share, the company commands a market capitalisation of about $1.58trn. But investors may still be underestimating the role the firm could play in the next stage of AI infrastructure. A price closer to $1,000—implying roughly a tripling in value—no longer seems implausible if current industry trends hold.

The key lies in how hyperscale cloud providers—Microsoft, Amazon, Google and Meta—are reshaping their computing stacks. Nvidia’s GPUs dominate the training of AI models, a compute-intensive process that benefits from flexible, general-purpose hardware. But once models are trained, they must be deployed across billions of queries each day. That is the world of inference, where efficiency, cost and power consumption matter far more than raw versatility.

Custom-designed chips—known as ASICs—are increasingly suited to this task. Unlike Nvidia’s universal GPUs, ASICs are built for specific workloads, allowing hyperscalers to reduce energy consumption and dramatically lower the cost of running AI applications. As AI usage explodes, the economics of inference may become decisive.

This is where Broadcom sits in a particularly advantageous position. The company has quietly become the industry’s leading designer of custom AI silicon and high-speed networking infrastructure. Many hyperscalers, eager to reduce dependence on Nvidia’s expensive GPUs, are developing their own chips—and Broadcom frequently serves as the engineering partner behind them. Each hyperscale data centre requires not only compute but also enormous volumes of networking equipment, another Broadcom speciality.

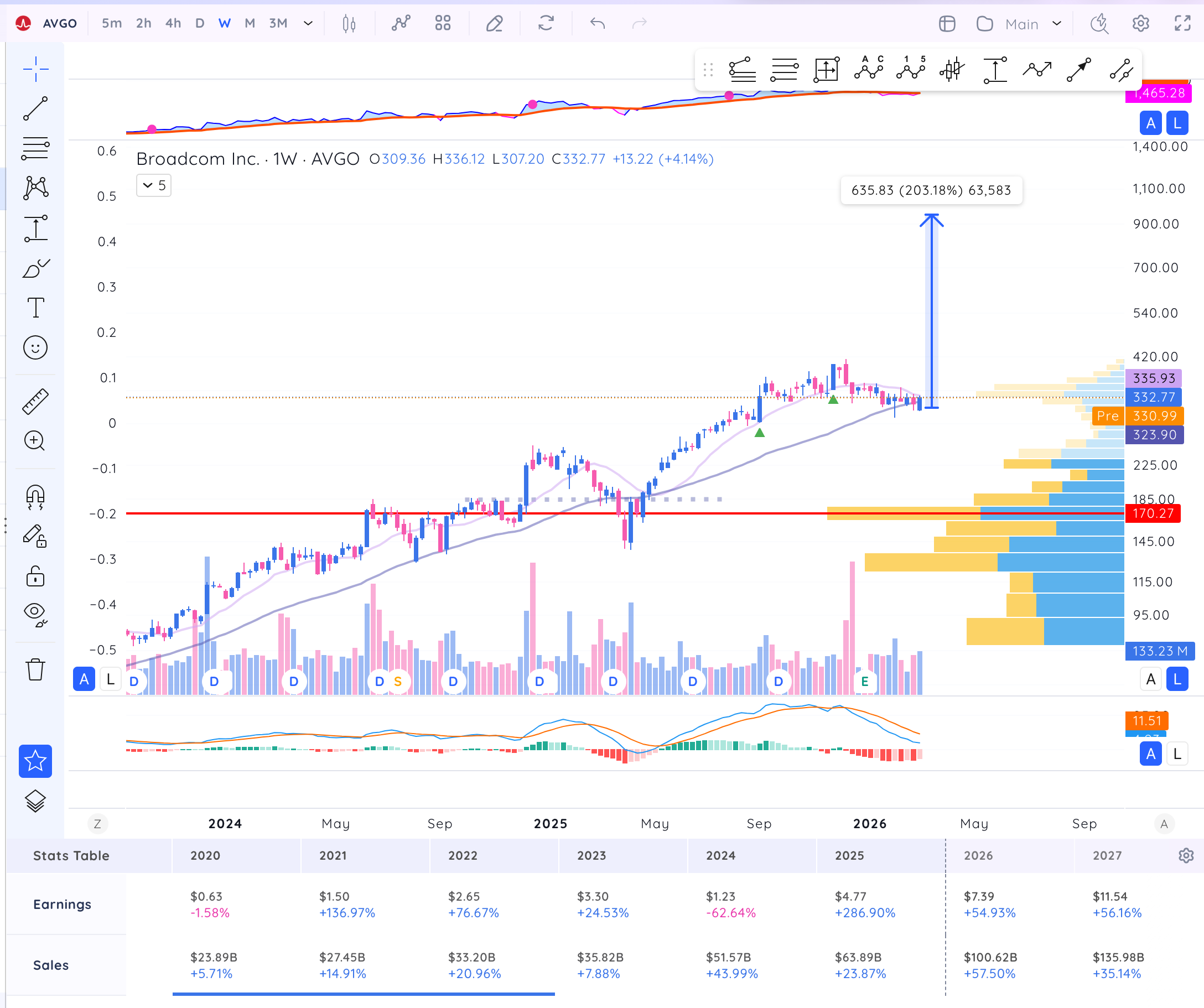

For two quarters now, the business (orange line, FCF/share) has been inflexing higher while sentiment (blue line, valuation, EV/Sales) has been discounting some AI overspending fears.

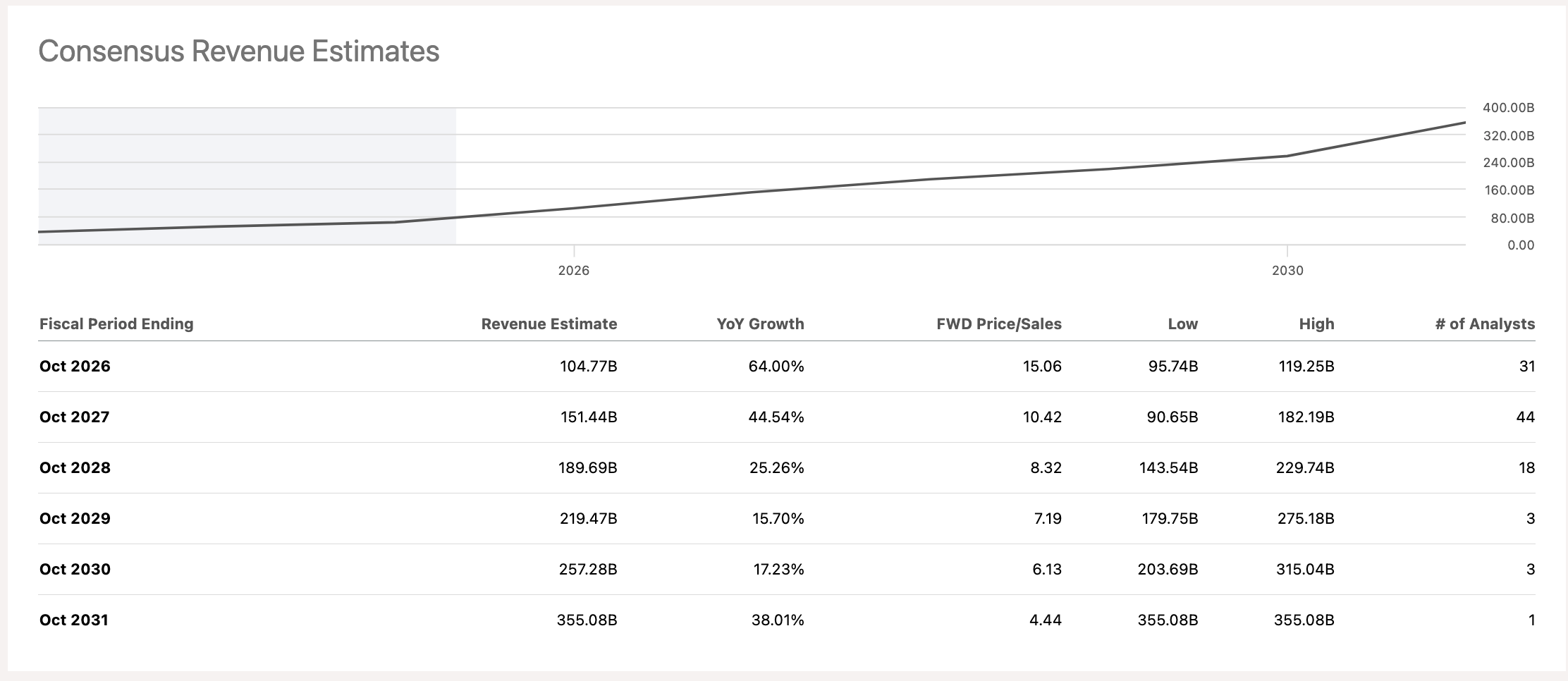

The scale of the opportunity is enormous. Hyperscale AI capital expenditure could approach $400bn–$500bn annually by the late 2020s. Broadcom itself has suggested its AI semiconductor revenue could exceed $100bn by 2027. If such figures materialise, the firm would possess an AI business rivaling Nvidia’s in size.

Markets, however, still see Nvidia as the sole sovereign of the AI revolution. History suggests that technological booms rarely produce just one king. If Nvidia built the engines of AI training, Broadcom may yet build the infrastructure on which the entire AI economy runs.