Buffett bought it. The market forgot it. Someone may soon be reminded.

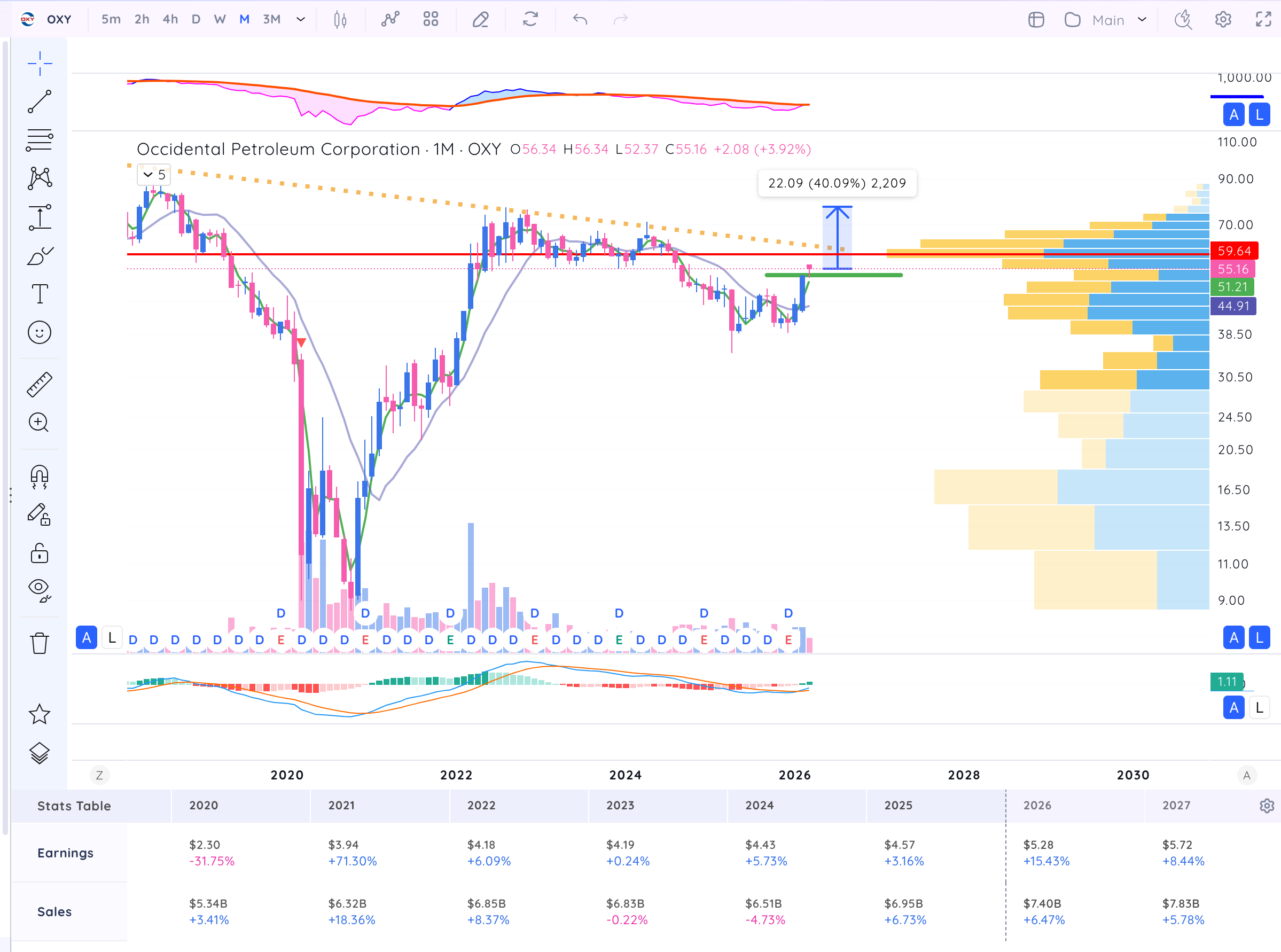

After a spectacular rise from $10 to $77 between 2020 and 2022, Occidental’s shares have spent three years doing what oil companies do best when the cycle turns against them: declining. The culprit is familiar — a $12 billion acquisition (CrownRock, 2023) that loaded the balance sheet with debt precisely as crude prices normalised. The stock sits near $55, with a wall of resistance at $60 that the market has refused to breach. The chart looks like a company still serving its sentence.

The thesis for optimism is not about oil prices. It is about arithmetic.

Management has done something rare: it has given investors a quantified, endogenous catalyst. The sale of OxyChem in January 2026 accelerated deleveraging, cutting principal debt from $25 billion to $15 billion in twenty months.

A $700 million tender offer will push that figure to $14.3 billion before mid-year.

The mechanical consequence is $365 million in annual interest savings — before a single extra barrel is pumped.

Add $500 million in structural cost reductions across oil and gas operations and $400 million in midstream optimisation, and management’s guidance points to a $1.2 billion improvement in free cash flow in 2026 alone.

None of this requires WTI to rally. It requires only execution — which, in 2025, Occidental delivered in excess of every guidance metric it set.

The observable signal is prosaic but precise: lease operating expense per barrel below $8.00 when first-quarter results land on 7th May 2026. If that number prints, the efficiency narrative becomes undeniable. If it does not, the next test arrives when STRATOS — the world’s largest direct air capture facility — begins commercial operations in Q2, offering the market a rather more exotic re-rating story.

The risk is equally legible. WTI below $55 sustained, or an operational stumble in the post-CrownRock integration, would delay everything. A winter storm already clipped first-quarter volumes.

The sentence, in short, may be nearly served. The $60 wall is both a technical resistance and a fundamental referendum — one that May’s earnings call is well positioned to deliver a verdict on.